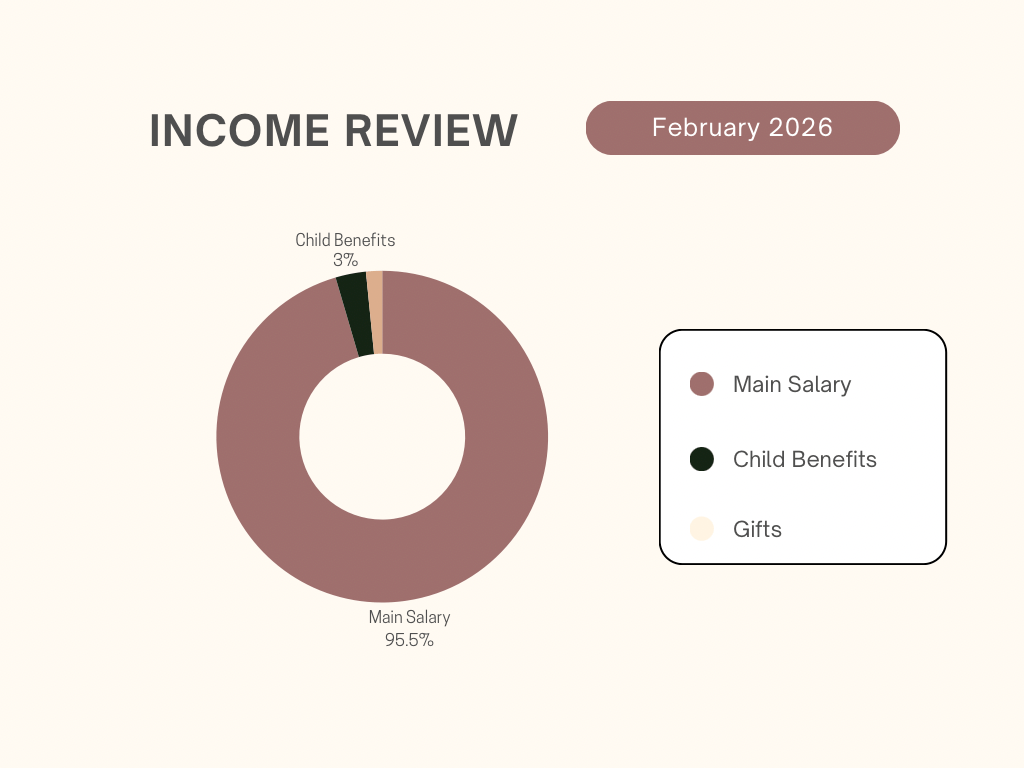

Since I’ve decided to be more mindful with my spending, I will share my monthly expenses with you all throughout 2026. Here’s the breakdown for February.

Income: 2778$

Job salary: 2733$

Child benefits: 85$

Gifts: 45$

Spending: 3020$

Right away, this is not a good sign. We can clearly see that I spent more than I earned. My goal is to spend less and save 10% of my income.

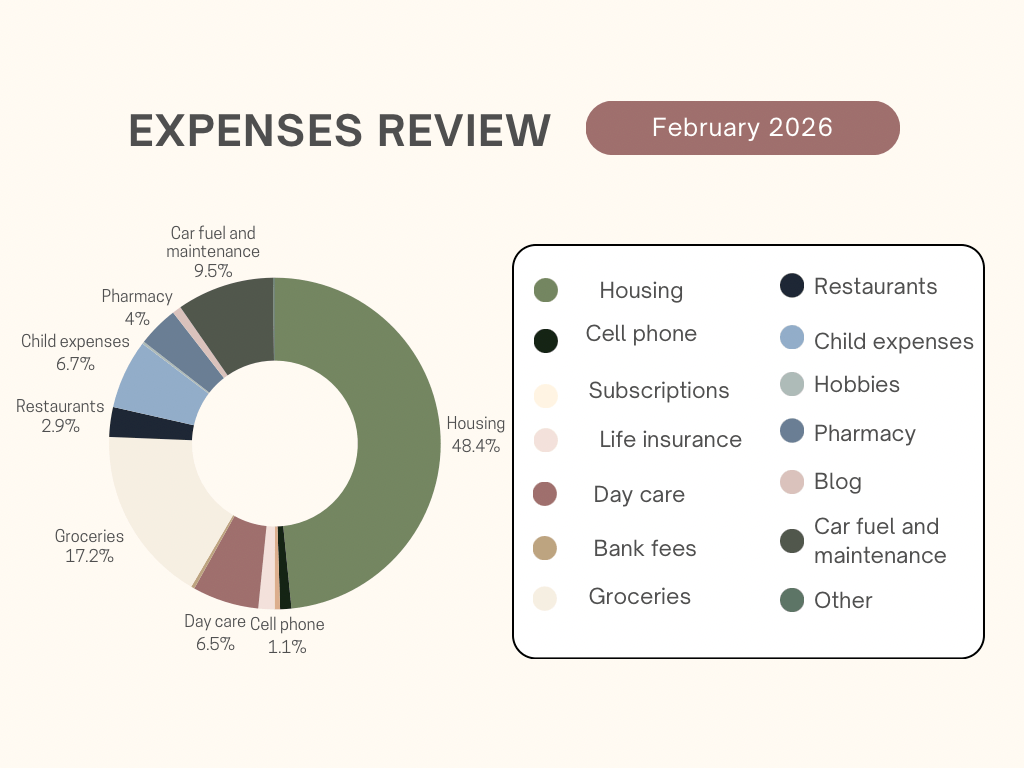

Bills: 1750$

Housing: 1450$

* Every expense related to housing is typically paid from my partner’s and my joint account. This includes mortgage payments, electricity, and Wifi bills. It also covers taxes, minimum debt payments, house and car insurance, and some shared expenses for my daughter. This amount represents my portion of the payments, with each of us paying half of every bill.

Cell phone: 33$

Disney+ subscription: 11$

iCloud subscription: 5$

Life insurance: 47$

Day care: 194$

Bank fees: 10$

Variable expenses: 1270$

Groceries: 388$

Restaurants: 87$

Car fuel: 279$

Expenses for my daughter: 202$ (we loaded up on diapers because there was a good sale)

Expenses for the house: 7$

Hobbies: 7$

Pharmacy: 119$

Costco: 128$

Other: 5$

Blog related expenses: 26$

Car maintenance: 5$

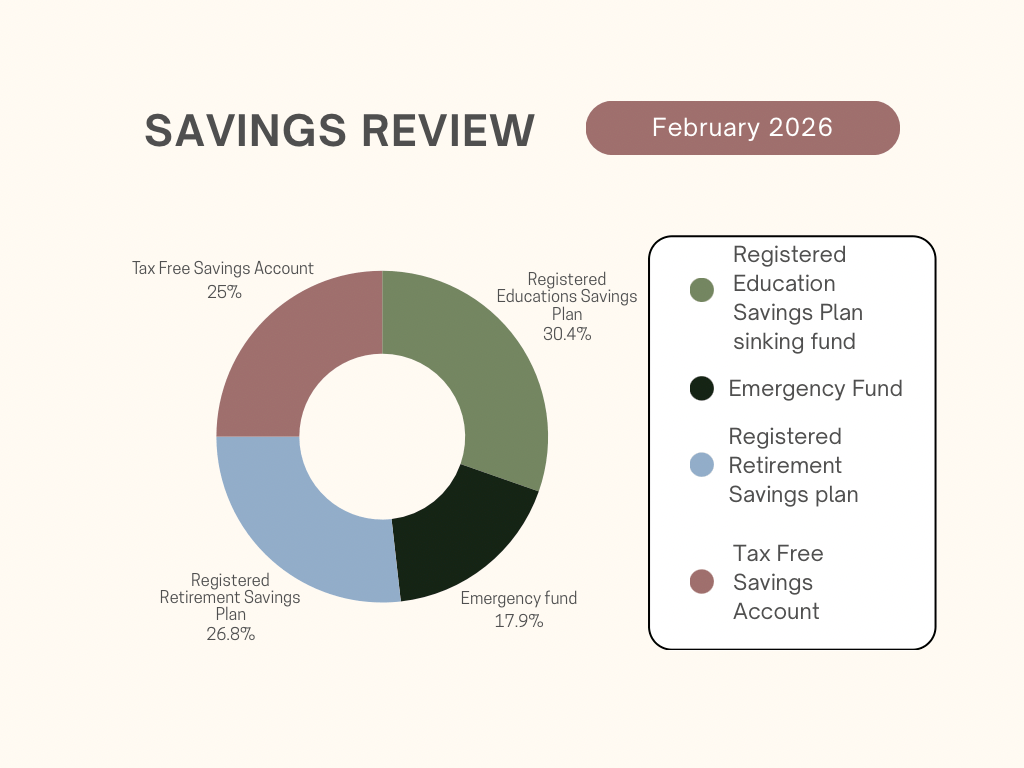

Savings : 280$

I did pay more than expected. However, I still managed to put some money aside into my savings. The extra money came from my sinking funds.

Daughter’s Registered Education Savings Plan sinking fund: 85$

Emergency fund: 50$

Registered Retirement Savings Plan: 75$

Tax Free Savings Account: 70$

This is my spending review for February. I haven’t reached my goal because I still spent more money than I earned this month. For March, I also have a few significant purchases coming up. These include my professional association dues. I need to make spring and summer purchases for my daughter. Additionally, I plan to buy a bike buggy for our upcoming bike rides this summer.

How was your spending for February? Did you stay within your budget? Don’t hesitate to let me know!